A private-label buyer sits down in January 2026 to plan next year’s HEPA filter line. Tariffs on Chinese imports have been cut to 10% since the November 2025 truce, but that truce runs out on November 10, 2026. Reshoring headlines promise cheaper, closer factories. So the buyer asks the obvious question: lock in a China supplier now, or start qualifying a U.S. one before the window closes?

That question drives more sourcing decisions this year than any other single factor in the filtration industry. And the honest answer isn’t “China” or “U.S.” — it’s whatever the numbers below say for your specific order size, certification needs, and timeline.

The Real Question in 2026 Isn’t “Leave China or Not”

Here’s what actually happened to trade policy. In November 2025, Washington and Beijing agreed to hold the reciprocal tariff rate at 10% (down from a peak of 125%) through November 10, 2026. At the same time, 178 separate Section 301 product exclusions were extended to that same date. Filtration components imported under air-purifier and machinery-parts codes still carry additional Section 301 duties layered on top of that baseline — so total landed cost varies by HS code, not by some flat “China tax.”

That single expiration date, November 10, 2026, is why most buyers aren’t asking whether to leave China. They’re asking how to structure contracts so a policy reversal next winter doesn’t wreck their landed cost math. A diversified supplier base, flexible MOQs, and contracts that separate FOB pricing from duty exposure matter more right now than picking a country and hoping.

What is the actual manufacturing cost?

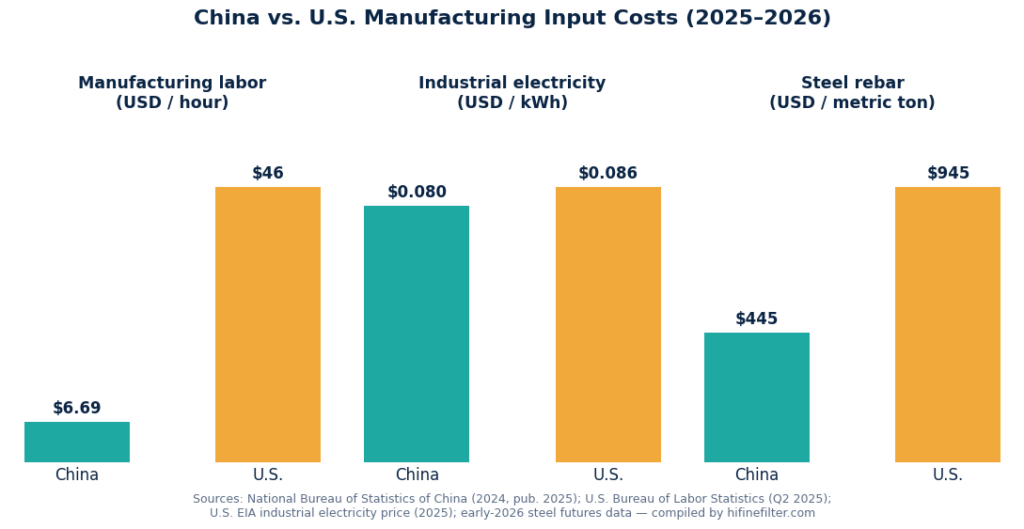

Start with labor, because it still explains most of the price gap between a Chinese-made and U.S.-made filter cartridge.

| Cost input | China (2025–26) | United States (2025–26) | Gap |

|---|---|---|---|

| Manufacturing labor, fully loaded | $6.69 / hour | $45.65 / hour | ~6.8x |

| Industrial electricity | $0.080 / kWh | $0.086 / kWh | Roughly even |

| Steel rebar, per metric ton | ~$445 | ~$945 | ~2.1x |

That electricity row surprises most people. China’s grid-cost edge, the one everyone assumes still exists, has narrowed to almost nothing on paper. The gap that hasn’t closed is labor, and it isn’t closing anytime soon — China’s own labor cost index kept climbing through 2026, but off a base low enough that the multiple still sits near 7x.

Reshoring supporters point out, correctly, that a 25%+ tariff stack can erase a chunk of that labor advantage on paper. What gets left out is the other side of the U.S. cost equation: workforce. A 2026 manufacturing outlook study from CADDi and SME found that 79% of U.S. manufacturing executives rank the skilled-labor shortage as their single biggest operating challenge, and separate industry tracking counted roughly 601,000 unfilled U.S. manufacturing positions this year. The Reshoring Initiative’s own 2025 survey found something counterintuitive: OEMs said they’d bring back 30% more production if skilled labor were simply available — more than the 23% they’d reshore from a 15% tariff increase. Labor availability, not tariffs, is the tighter constraint on “just build it in America.”

Where Chinese HEPA Manufacturers Still Win

Cost is only half the picture. The other half is whether a factory can actually build what a private-label brand needs, at the volume it needs, on the timeline it needs.

China’s filtration manufacturing sits inside dense industrial clusters — Guangdong’s Pearl River Delta for electronics-adjacent filter media, Zhejiang’s Ningbo region for textile-to-filter verticals, and Hebei and Jiangsu for high-volume nonwoven and glass-fiber media production. Buyers sourcing in these clusters commonly report 20–35% total cost efficiency versus Western equivalents, driven less by wage arbitrage alone and more by having every input — raw media, frames, gaskets, packaging — within a short trucking radius of the assembly line.

Low MOQs Matter More for Private Label Than People Admit

For a private-label or wholesale buyer testing a new SKU, minimum order quantity is often the real deciding factor, not unit price. A factory with vertically integrated OEM/ODM filtration solutions can typically accommodate smaller pilot runs and custom tooling for new housing shapes far faster than a U.S. facility built around long production runs of standardized parts. That flexibility is what lets a distributor launch a branded H13 line without committing to a container-load minimum on day one.

Does “Made in China” Still Mean Certified?

This is where a lot of buyers get nervous, and where the market has genuinely changed. “Made in China” and “certified to international HEPA standards” are two separate questions, and conflating them is how buyers end up with a customs problem.

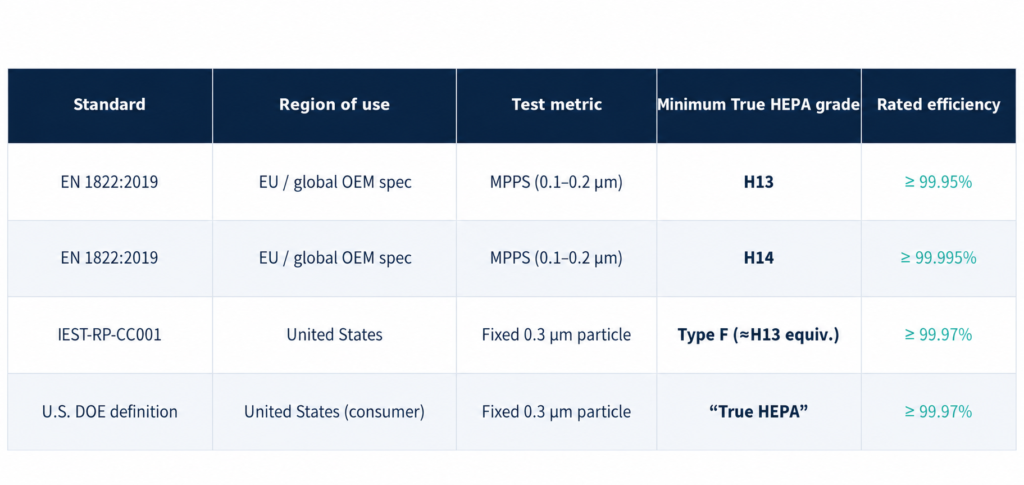

The EU standard, EN 1822:2019, grades filters against the Most Penetrating Particle Size rather than a fixed particle diameter, with H13 as the accepted “true HEPA” floor and H14 as the higher industrial-cleanroom grade. The U.S. framework, IEST-RP-CC001, along with the Department of Energy’s consumer “True HEPA” definition, tests at a fixed 0.3-micron particle and requires ≥99.97% capture. In an absolute sense, neither of these two standards is “more difficult”; they are different measurement concepts, but the results just happen to be very close.

What separates a compliant factory from a risky one isn’t the standard on the label. It’s whether a factory holds ISO 9001 quality management certification and can hand a buyer real third-party test reports — not marketing copy — for every batch. We’ve broken down exactly how HEPA grades translate across standards and how to specify a testable grade instead of a vague “HEPA” claim when writing a purchase order — the difference between those two approaches is often what shows up, or doesn’t, in a customs audit.

How the Market Is Shifting Through the Rest of 2026

The demand side of this story is not slowing down. The global HEPA filter market grew from $5.38 billion in 2025 to an estimated $5.87 billion in 2026, and independent market research projects it reaching $9.88 billion by 2032 — a 9.06% compound annual growth rate. Asia-Pacific remains both the fastest-growing demand region and the dominant production base.

Two structural shifts are worth watching inside that growth curve. First, China tightened its own Work Safety Law in 2025–2026, requiring manufacturers to fund dedicated workplace-safety programs — a change that raises the compliance bar for smaller workshops and tends to favor established, audit-ready factories over informal ones. Second, smart filtration is moving from novelty to spec sheet: IoT-enabled filter-life sensors and real-time air-quality monitoring are increasingly requested features in OEM contracts, not optional add-ons.

So, Which One Should You Actually Pick?

Neither country wins this outright, and treating it as a binary choice is where most sourcing strategies go wrong. A workable framework looks like this:

- High-volume, cost-sensitive private label: China’s cluster manufacturing and lower MOQs still win on landed cost, even with current tariffs factored in.

- Certification-critical or IP-sensitive components: verify ISO 9001 status and demand batch-level EN 1822 or IEST-RP-CC001 test reports regardless of country; this is a supplier-quality question, not a geography question.

- Time-sensitive or politically exposed contracts: build in dual-sourcing or flexible FOB terms so a November 2026 tariff reset doesn’t strand your pricing.

For most brands building or expanding a private-label filtration line, the practical move isn’t picking a flag. It’s picking a factory that can document its certifications, hit a realistic MOQ, and absorb tariff volatility without passing all of it downstream. That’s the conversation worth having before the next contract gets signed.